Preferential tax rates in Europe

EU countries have high taxes. For example, the maximum income tax rate is 44% in Greece and 48% in Portugal. But residents can optimise their taxes through special tax regimes. See how to reduce the amount of tax payments in European countries.

2 main things that affect income tax in Europe

Double tax treaties (DTTs) are agreements between states. They regulate taxation for people and companies that earn income in one country and, at the same time, are tax residents of another.

DTTs allow investors to reduce their tax burden: they do not need to pay taxes in two countries in full.

As a rule, European states have DTTs with many countries, making the tax jurisdiction change more profitable. Thus, Malta has signed DTTs with 76 countries, while Portugal has 81 agreements.

Domicile affects the tax base and rates. This concept implies the country of permanent residence. Domicile is assigned at birth, most often according to the father’s domicile; it can be changed over a lifetime.

To obtain domicile in the chosen country, one usually must fulfil several conditions. For example, you need to live for 17 years in Cyprus. In Malta, you need to break ties with other countries and confirm your intention to return to the country in the future.

A person domiciled in a certain country can be its tax resident or non-resident. Relocation for several months or years rarely results in a change of domicile.

In some states, non-domicile tax residents enjoy tax benefits offered under the residence by investment programs.

Non-Habitual Resident in Portugal

Non-Habitual Resident in Portugal

An investor with a Portugal residence permit can apply for the Non-Habitual Resident (NHR) status if they move to the country. This status allows the holder to reduce income tax in Portugal and not pay taxes on their global income.

The preferential tax status is valid for 10 years. It is only available to new tax residents.

A highly qualified specialist pays a flat 20% income tax on their salary or income earned as self-employed. The standard rate is calculated on a progressive scale and reaches 48%.

The tax rate for pensions from other countries is 10%.

Sometimes, NHRs don’t need to pay taxes on income from employment, dividends, interest, rent and capital gains from abroad. For income to be tax-free, the following conditions must be met:

Income tax has already been paid in another country.

Portugal and the income source state have a double tax treaty (DTT) or the OECD Model Tax Convention on Income.

The source of dividends, interest, rent or the self-employed person’s income is not in an offshore jurisdiction.

To get the NHR status, you must become a Portuguese tax resident. It is possible if the investor spends at least 183 days a year in Portugal. A day of stay counts only if you spend the night in the country. Thus, the day will not count for tax residence if you arrive in the morning and leave in the evening.

The investor must get a Portuguese taxpayer number and the status of a tax resident and apply for the special tax status before March 31st of the next year.

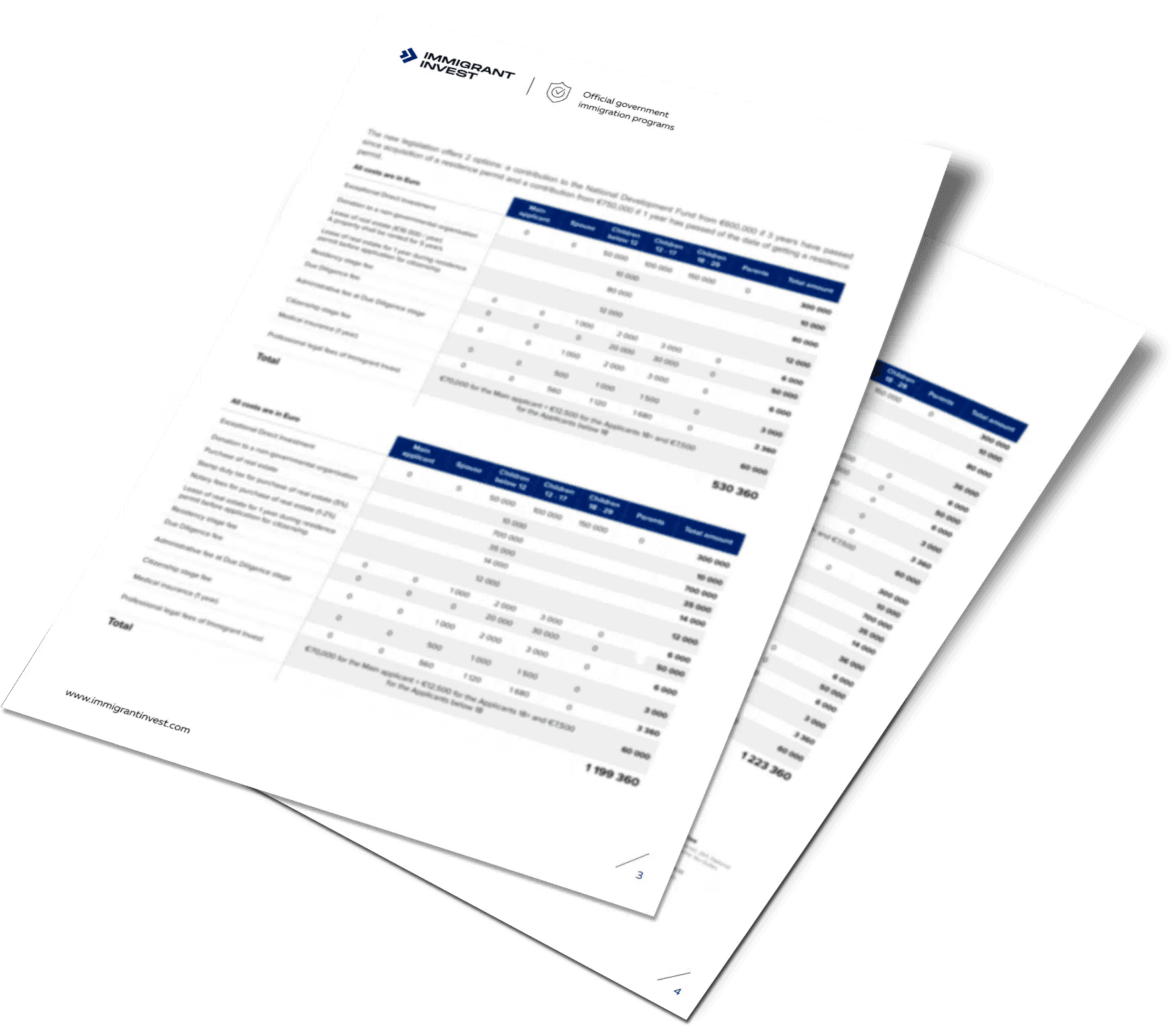

Individual cost calculation of the residence permit in Portugal

Taxes for non-domicile residents in Cyprus

Taxes for non-domicile residents in Cyprus

Cyprus permanent residence allows you to become a non-domicile tax resident and enjoy benefits.

Cypriot tax residents without domicile in the country don’t pay the Special Defense Contribution to the budget on dividends, interest and rental income from abroad.

Income tax is levied at 0 to 35%. The rate depends on the annual income:

0% — up to €19,500;

20% — €19,501 to €28,000;

25% — €28,001 to €36,300;

30% — €36,301 to €60,000;

35% — over €60,000.

Tax residents must pay the tax on income earned in Cyprus and abroad.

Profits from the sale of securities are not subject to income tax. Capital gains tax is paid when selling real estate in Cyprus with a profit; the tax base is the difference between the sale and purchase amount, and the rate is 20%.

To become a Cypriot tax resident, you must meet the following conditions:

live in Cyprus for more than 60 days a year;

not spend more than 183 days a year in other countries;

buy or rent housing in Cyprus;

do business or work in Cyprus.

Non-domicile residents are people who weren’t born in Cyprus and have not lived there for more than 17 years out of the last 20 years.

Individual cost calculation of the Cyprus permanent residence

Malta residence permit for tax optimisation

Malta residence permit for tax optimisation

In Malta, investors can get a residence permit, permanent residence or citizenship by naturalisation for exceptional services by direct investment. A special tax regime is provided only for investors with residence permits. Citizens of non-EU countries obtain them through the Malta Global Residence Programme.

The tax on income from foreign sources received in Malta is 15%. The minimum tax amount is €15,000 per year.

There is no tax on income earned abroad and not transferred to Malta. Income derived from Maltese sources is subject to income tax at 35%.

The following applicants can participate in the Malta Global Residence Programme:

an investor with legal income enough to support their family;

without criminal records;

with health insurance valid in the EU;

with proficiency in Maltese or English at a conversational level.

A spouse, children under 25 and other financially dependent relatives (namely, parents, grandparents or siblings) can get residence permits with the main applicant.

To obtain a residence permit, an investor buys a property for at least €220,000 or rents housing for at least €8,750 per year. They also pay an administrative fee of €5,500 if the investor purchased property on the island of Gozo or in the south of Malta or €6,000 in other cases.

It is optional to live in the country to maintain tax residence and retain a residence permit in Malta. But you can not spend more than 183 days a year in any other country.

No special tax benefits exist for investors with Malta permanent residence or citizenship obtained for exceptional services by direct investment. They spend at least 183 days a year in the country to become Maltese tax residents.

Income tax for residents without benefits is calculated on a progressive scale. The rate is up to 35%. The tax amount depends on the family composition and tax deduction. The deduction is up to €9,905 per year.

Malta permanent residence or citizenship doesn’t oblige the investor to become a tax resident. Non-residents pay tax only on income earned in Malta. The income tax rate is up to 35%; it depends on the annual income.

Taxes for non-domicile residents in Greece

Taxes for non-domicile residents in Greece

Wealthy foreigners can pay taxes in Greece under a special Non-Domiciled Tax Regime. It is valid for 15 years.

Taxes for investors with Greek non-domicile resident status are the following:

€100,000 — a flat tax on global income;

€20,000 — a contribution for a close relative who obtains the special tax status with the investor;

9% to 44% — a tax on salary or income from commercial activity earned in Greece;

15% to 45% — a tax on property income earned in Greece;

no taxes on inheritance and gifts for foreign assets.

The conditions for obtaining a special tax status are the following:

living in Greece for at least 183 days a year;

not being a Greek tax resident for at least seven years out of the last eight;

investing at least €500,000 in real estate, securities or business in Greece.

Participants of the Greece Golden Visa Program are not subject to the condition of investing in assets in the country as they fulfil it when they apply for a residence permit.

Individual cost calculation of the residence permit in Greece

Highlights about European taxes for investors

Taxes in Europe tend to be quite high, but they can be optimised through special tax regimes, deductions and other incentives.

The ability to optimise taxation is affected by various factors: for example, the existence of a DTT between the country of residence and the country of income, as well as the taxpayer’s domicile.

Conditions for new tax residents in European countries are more favourable than for people who have lived there for a long time.

Countries with residency investment programs, like Portugal, Cyprus, Malta, and Greece, offer new residents special programs with reduced rates or flat taxes.

To take advantage of the preferential regimes, you must become a tax resident of the country. Usually, you must live in the country for at least 183 days a year, but there are exceptions. For example, moving to Malta is unnecessary to maintain a special tax status under the Global Residence Program.

Practical Guide

Comparison of citizenship and residency by investment programs

Material prepared by an expert

Albert Ioffe

Legal and Compliance Officer

Frequently asked questions

Taxes for individuals in the UAE and Turkey