How to optimise your tax liabilities through a second citizenship and residency

An individual can optimise their tax liabilities by changing their country of tax residency or registering a company abroad. To do this, they need to hold a residence permit, permanent residency, or second citizenship.

Discover the countries where an investor can obtain a residence permit, permanent residency, or citizenship in order to reduce the tax due on their global income, get a refund of up to 100% of the corporate tax paid, or receive an exemption from paying corporate tax for 50 years.

Author •Albert Ioffe

Explains how to legally reduce your tax burden

How to optimise your tax liabilities through a second citizenship and residency

What is tax optimisation?

Tax optimisation involves measures that reduce the taxes an individual or a company pays, freeing up money for business development and other needs.

One of the goals of tax optimisation is to minimise tax liabilities, and this can be achieved by an individual moving to another country or opening a company abroad.

Although taxes are high in such countries as the United States, the UK, and most EU member states, other countries attract investors by offering preferential treatment to reduce their tax burden.

We do not recommend or discuss any of the illegal or criminal ways of reducing taxes, such as splitting a company into several legal entities or money laundering through fictitious transactions. These methods can result in administrative and criminal liability for tax evasion, with those convicted facing prison sentences and being barred from holding public positions or serving as company directors.

In this article, we consider only legal methods of tax optimisation: choosing a special tax regime, opening a company abroad, and changing the country of tax residency.

How to legally optimise taxation

Check your counterparties. If a counterparty has been involved in fraud or tax evasion, the costs of transactions with them may not be taken into account when calculating the tax base. In such cases, the company will have to pay more taxes than if the costs had been deducted.

Engage in charity work. In many countries, individuals and companies are entitled to tax breaks when they donate money to charity. For example, in the United States, a taxpayer can deduct up to 60% of their adjusted gross income for cash contributions to public charities and operating foundations.

Change the country of tax residency. Sometimes, moving your tax residency to another country can help reduce the tax burden. For example, Antigua and Barbuda has no income tax, and International Business Companies there are exempt from taxes on global income for 50 years.

To become a tax resident of a country, one is normally required to live there legally for at least 183 days a year. However, there are exceptions: for example, in Cyprus, one can become a tax resident in 60 days, provided that they do not live in any other country for 183 days a year. They must also have a job and a permanent home on the island.

For companies to be recognised as tax residents of a country, they must be incorporated in it or have their central management and control located there.

Choose a favourable tax regime. In some countries, tax residents can choose how to pay taxes on certain types of income. In Malta, property owners pay tax on rental income at a progressive rate of up to 35% or use a special tax scheme at a flat rate of 15%.

When moving to Greece, Portugal, or Cyprus, foreigners can minimise their taxes through special tax regimes. For example, in Greece, foreign nationals can benefit from a 50% income tax break on their annual salary or business income for 7 years after relocating to the country.

Take advantage of benefits and deductions. These allow reducing the tax base and having a part of the paid tax refunded. For example, Hungary provides tax relief for workers under 25, recently married couples, families with children, and retired employees who continue working.

Taxes in the Caribbean

Antigua and Barbuda, Grenada, Dominica, St Lucia, and St Kitts and Nevis are Caribbean countries with citizenship by investment programs. Obtaining second citizenship in any of these countries allows one to register a company and become a tax resident there, which can often reduce one’s tax liabilities.

There are no inheritance or capital gains taxes in the Caribbean countries, and some of them don’t even have an income tax.

Taxes for individuals. There is no income tax in St Kitts and Nevis and Antigua and Barbuda. Elsewhere in the Caribbean, this tax is charged according to a progressive scale.

The tax base can be different: in Dominica, tax residents pay tax on their global income, and non-residents pay tax on the income earned in Dominica.

In addition to income tax, residents pay real estate tax, tax on transfer of ownership when selling real estate, and stamp duty. Tax rates vary by country and situation.

Income and property taxes in the Caribbean

Country

![]() Antigua and Barbuda

Antigua and Barbuda

Income tax rate for residents

Not charged

Income tax rate for non-residents

Not charged

Tax rates for property owners

0.1—0.5% as property tax

10—20% as land tax

Country

![]() Grenada

Grenada

Income tax rate for residents

10—30%

Income tax rate for non-residents

15% on income earned in Grenada

Tax rates for property owners

0.2—0.5% as property tax

0,2% as residential land tax

0,3% as building tax

Country

![]() Dominica

Dominica

Income tax rate for residents

15—35% on income earned in Dominica and globally

Income tax rate for non-residents

15—35% on income earned in Dominica

Tax rates for property owners

1,27% as annual municipal tax

Country

![]() St Kitts and Nevis

St Kitts and Nevis

Income tax rate for residents

Not charged

Income tax rate for non-residents

Not charged

Tax rates for property owners

0.2—0.5% as property tax

Country

![]() St Lucia

St Lucia

Income tax rate for residents

0—30% on income earned in St Lucia

Income tax rate for non-residents

10—30% on income earned in St Lucia

Tax rates for property owners

0.25—0.4% as property tax

Taxes for business. In most Caribbean states, companies pay income tax on their global income and VAT. To operate, International Business Companies, known as IBCs, must have an office or a licensed representative in the country.

The Caribbean countries do not levy withholding taxes on dividends, royalties and interest when they are paid to residents of the country. The exception is St Lucia, which has a 10% tax on interest and royalties.

Taxes for companies registered in the Caribbean

Country

![]() Antigua and Barbuda

Antigua and Barbuda

Corporate tax

25%

VAT

0 to 17%

Country

![]() Grenada

Grenada

Corporate tax

28%

VAT

0 to 20%

Country

![]() Dominica

Dominica

Corporate tax

25%

VAT

0 to 15%

Country

![]() St Kitts and Nevis

St Kitts and Nevis

Corporate tax

33%

VAT

0 to 17%

Country

![]() St Lucia

St Lucia

Corporate tax

30%

VAT

0 to 12,5%

Taxes in Vanuatu

Vanuatu offers one of the most beneficial taxation regimes both for individuals and companies. There are equal terms for residents and non-residents, including citizens who spend more than 183 days outside the country.

For individuals, the following sources are exempt from taxes:

personal income;

real estate ownership;

wealth;

inheritance;

capital gains;

capital export.

Inhabitants only pay a 12,5% value-added tax which is already included in the price of goods and services.

Legal entities residing in Vanuatu are exempt from paying corporate taxes for 20 years after registration. Instead, they pay an annual registration fee of $300.

Taxes in EU countries

Taxes are quite high in the European Union. For example, the income tax rate can reach 44% in Greece, and 48% in Portugal. However, there are various ways of reducing tax liabilities, such as exercising one’s right to a tax deduction or obtaining a preferential tax status.

Malta. Income tax in Malta is levied on a progressive scale, ranging from 0 to 35%.

Tax residents benefit from a tax deduction of up to €9,905, depending on the income and marital status of the taxpayer.

VAT in Malta is 18%, one of the lowest rates in the European Union; only Luxembourg and Switzerland have lower VAT rates in Europe.

To become a tax resident in Malta, an individual needs to reside in the country for at least 183 days a year. However, an exception is made for holders of residence permits obtained by investment. Such foreigners immediately become tax residents and do not need to live in Malta, as long as they do not spend 183 days a year in any other country.

Investors with Maltese residency pay taxes under a special tax regime:

15% on income earned abroad and transferred to Malta;

35% on income earned in Malta.

Malta Global Residence Programme participants pay income tax of at least €15,000 per annum on income transferred to Malta. Those who do not pay this minimum amount are not allowed to extend their residence permits. There is no tax charged on income which was earned abroad and not transferred to Malta.

Companies in Malta pay corporate tax at a rate of 35%. Part of the paid tax can be refunded to shareholders:

100% if the holding company owns a share in a foreign company and belongs to the Participating Holding category;

6/7 if the company is trading;

5/7 if the company profits from royalties and interest;

2/3 if the company receives income from a country having a double taxation agreement with Malta.

Portugal offers a special tax regime for skilled professionals moving to the country to pursue employment or self-employment in fields such as higher education, scientific research, technology, and startups.

If approved, candidates have their personal income taxed at a flat rate of 20% and receive an exemption for foreign income for 10 years. To qualify, they also must not have been residents of Portugal in the preceding 5 years.

Tax on dividends, interest, royalties, capital gains, and rental income received abroad does not have to be paid at all. For this rule to apply, the country of the income source must have a tax agreement with Portugal and not be considered an offshore jurisdiction.

Greece offers three special taxation regimes for foreigners who obtain a residence permit in the country.

New Greek residents who are employed by a local company, self-employed, or run a business in the country can be exempt from paying taxes on 50% of their income for 7 years.

The foreign pensioners’ regime allows retirees to pay a 7% tax on their income from a foreign source for 15 years after relocating to Greece.

Finally, those who invest at least €500,000 in the country’s economy are eligible for the high-net-worth individual regime. Instead of regular taxes, they can pay a lump sum of €100,000 every year, regardless of their income.

In Cyprus, tax benefits can be received by residents not domiciled in the country. Non-domiciled residents are considered to be those individuals who have lived in Cyprus for less than 17 of the last 20 years and were not born in this country. Such residents do not pay tax in Cyprus on their global income, dividends, interest, and capital gains from the sale of securities and corporate rights.

Foreigners can become tax residents in Cyprus by living in the country for at least 60 days. One will also need to buy or rent real estate in the country and either run a business or work there. At the same time, they cannot spend more than 183 days a year in any other country.

Hungary levies a 15% personal income tax on all residents, which is one of the lowest taxes in Europe. Additionally, there are multiple tax benefits and exemptions based on age, marital status, and other circumstances.

For example, a mother with at least four natural or adopted children is exempt from paying the tax on most of their income, such as their salary, entrepreneurial income, severance pay, sick pay, and childcare allowance.

Hungarian residents under the age of 25 do not pay income tax at all, while disabled people, newlyweds, and families with children may have their personal income tax reduced.

Hungary is also one of the most advantageous European countries to register a company. The 9% corporate tax rate is the lowest in the EU.

How to avoid paying taxes in two countries at the same time

Countries sign double taxation treaties, DTTs, that allow residents of the participating countries to avoid paying the full tax amount twice: in the country where the income is received and in the country of tax residence.

For example, if a UK tax resident rents out a property in Malta, they are exempt from paying tax on rental income twice thanks to a DTT between the two countries. Without a DTT, they would pay 15% tax on rental income in Malta and at least 20% in the United Kingdom. As a result of the DTT, they only need to pay 15% in Malta.

If a DTT between two countries does not exist, then taxes must be paid in both. For example, Vanuatu and the United Kingdom do not have a DTT. If a British investor becomes a tax resident of Vanuatu but does not transfer their business there, they will have to pay the full tax on their income in each country.

Some countries, such as the United States, the UK, Canada, and Singapore, offer foreign tax credits to mitigate potential double taxation, for both individuals and companies.

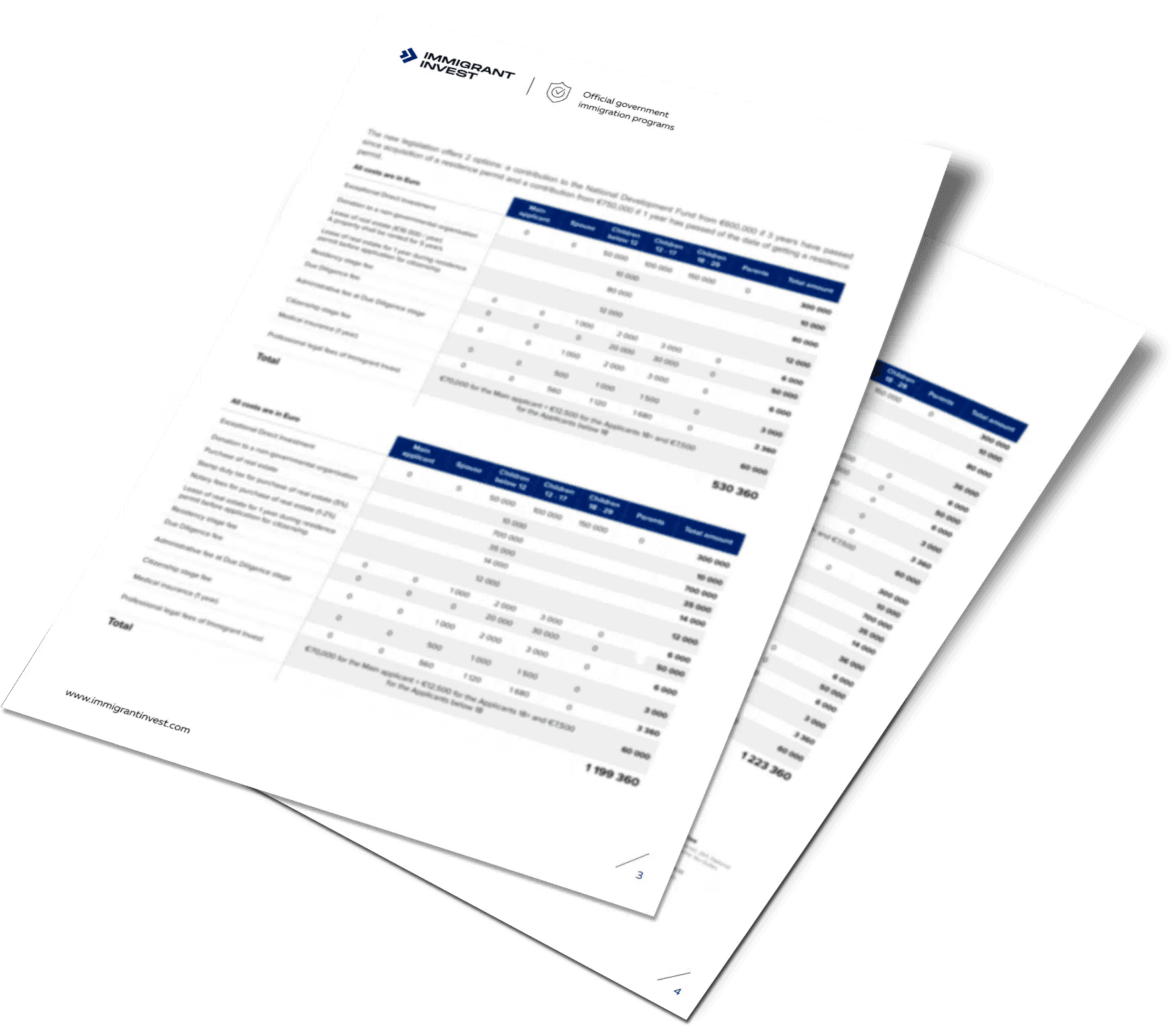

Where to obtain tax residency by investment for tax optimisation

In order to live permanently in another state, it is necessary to obtain a residence permit, permanent residency, or citizenship there. In some countries, citizenship or residency can be obtained by investment — and those often offer opportunities for tax optimisation.

Where can an investor get a residence permit, permanent residency, or citizenship

Country

Status

Citizenship by naturalisation for exceptional services

Investment

€690,000+

Processing time

1 or 3 years

Other strategies for tax optimisation

1. Tax-advantaged accounts. Using retirement and health savings accounts can help an individual reduce taxable income, and build savings for the future or withdraw cash for medical expenses tax-free. It is possible to open such accounts in many countries, including the USA, the UK, and Spain, although some of them place a limit on the amount of savings in these tax-preferred accounts.

2. Investment strategies. Investors can purchase municipal bonds, which are often tax-exempt, or choose investments that generate capital gains taxed at a lower rate than ordinary income. Alternatively, they can sell investments at a loss to offset capital gains, reducing overall taxable income.

3. Charitable donations. Contributing to donor-advised funds can help an individual get an immediate tax deduction while distributing donations over several years. In the United States, one can deduct up to 60% of their adjusted gross income for charitable donations.

4. Trusts. A taxpayer can set up an irrevocable trust to shift income to beneficiaries in lower tax brackets, reducing overall tax liability. St Kitts and Nevis is one of the countries with the most beneficial legal system for trustees.

5. Tax deductions and credits. A taxpayer can take full advantage of different deductions and credits, such as deductions on mortgage interest and medical expenses, or credits for education and energy efficiency.

Dual citizenship and taxes for US citizens

The United States is one of the few countries that taxes its citizens on their worldwide income, regardless of where they earn it or where they live.

However, some countries have treaties on the avoidance of double taxation with the USA, meaning that residents of those countries are taxed at a reduced rate or are exempt from double taxation on certain items of domestic income. There are over 60 countries on the list, including the EU member states, the UK, Canada, and China.

As the country recognises dual nationality, US citizens can obtain a passport from another state if the latter also allows it. For dual nationals whose second country does not have a tax treaty with the United States, the only way to avoid US taxation is by renouncing US citizenship.

Key things to know about tax optimisation

To legally optimise tax liabilities, one can change their country of tax residency or register a company abroad. This requires a residence permit, permanent residency, or second citizenship.

Certain countries, such as Antigua and Barbuda, St Kitts and Nevis, and Vanuatu, offer tax incentives for investors, including reduced or exempted taxes on global income or corporate profits.

Caribbean countries and some EU nations provide attractive tax benefits for investors through citizenship or residency by investment programs.

Immigrant Invest is a licensed agent for citizenship and residence by investment programs in the EU, the Caribbean, Asia, and the Middle East. Take advantage of our global 15-year expertise — schedule a meeting with our investment programs experts.

Frequently asked questions

Case studies

Antigua and Barbuda as a 4th citizenship: starting a business in the Caribbean

How to get a tourist visa to the USA for 10 years with the Antigua and Barbuda passport

Antigua and Barbuda citizenship for plans in the UK: studies, work, travel

Read also

Antigua and Barbuda Golden Visa: how to secure a Caribbean passport and achieve global mobility

Lyle Julien

17 best golden passports in 2024

Albert Ioffe

Top 27 best countries to retire for American expats

Alevtina Kalmuk