The Principality of Andorra is a small state in the Pyrenees, which is believed to be a true tax haven, especially compared to neighbouring Spain and France.

The legend is as close to reality as it can be. Thus, the first €24,000 of the income is tax-free, and the rest is charged up to 10%. The corporate tax is no bigger than 10%, while VAT is only 4.5%. Besides, Andorra doesn’t tax wealth and inheritance.

However, a shadow is hanging over the perfect picture as Andorra has double taxation treaties only with 10 countries.

Learn more about the effective rates, exemptions and special tax regimes to see if Andorra can ease your tax burden or not.

Overview of the Andorran taxation system

Andorran taxpayers are natural persons and legal entities. They can be either considered the country’s tax residents or non-residents. The status defines the applicable taxes and their rates.

Natural persons can become Andorran tax residents if they spend more than 183 days in 12 months in the country. Another ground for becoming a tax resident is having Andorra as the centre of your economic and vital activities.

However, a person isn’t considered an Andorran tax resident if they are a frontier worker who daily comes to Andorra from neighbouring Spain or France. The rule applies even if such frontier workers have been hired by a legal entity, which is an Andorran tax resident.

A company must meet at least one of the following criteria to be considered a tax resident:

-

be incorporated in Andorra;

-

have a registered office in Andorra;

-

the entity’s effective management is in Andorra.

Taxes are collected by municipalities and the government. Municipalities, or comús, are responsible for taxes on property, rental income, the establishment of commercial or business activities, and construction. The government collects personal income and corporate taxes, VAT, capital gains taxes, withholding taxes, and taxes on vehicle ownership.

The tax year for natural persons coincides with the calendar year. For legal entities, it is the same as the company’s accounting period but no longer than 12 months.

Currency. Andorra uses the euro as its official currency, though the country is not an EU member state. Thus, all taxes are calculated and paid in euros.

Foreign exchange control. The Andorran law doesn’t provide any foreign exchange regulations.

Exchange of tax information. Since 2014, Andorra has been committed to the OECD Declaration on Automatic Exchange of Information on Tax Matters. The Common Reporting Standard has been implemented since 2018.

Andorra has valid Tax Information Exchange Agreements with 24 countries and territories:

The Ukrainian Parliament has approved a Tax Information Exchange Agreement with Andorra, but the agreement hasn’t come into force yet.

New Tax Information Exchange Agreements are planned to be signed with Ecuador, Hong Kong, Macau, the Maldives, Morocco, Peru, and Samoa. However, it is yet unknown when they will come into force.

Trusted by 10,000+ investors

Sort out your tax obligations before it becomes a problem

Andorra’s income tax rates for residents and non-residents

Residents and non-residents pay different income taxes in Andorra, with varying taxable income rates and types. Personal income taxation is regulated with Law 5/2014 dated April 24th.

Impost sobre la renda de les persones físiques (IRPF) is an income tax paid by Andorran tax residents. It is levied on a progressive scale depending on the annual income amount, where the first €24,000 are tax-free.

Impost sobre la renda dels no-residents fiscals (IRNR) is an income tax for non-residents. The flat rate of 10% applies irrespective of the annual income amount.

Income tax rates for Andorran tax residents and non-residents

Residents pay taxes on their global income, while non-residents only pay taxes on income earned within Andorra.

The taxable income includes:

-

employment payments like wages;

-

income from entrepreneurial or business activities, including income earned by a company owner or manager;

-

royalties and the income derived from using immovable properties, like rental yields;

-

dividends and interest;

-

pensions and payments under life insurance or disability;

-

capital gains and losses.

Note that if dividends are received from an entity, which is an Andorran tax resident, such dividends are not taxed. But if a non-resident company pays dividends to Andorran tax residents, the dividends are subject to the income tax in Andorra.

The personal income tax must be filed and paid between April 1st and September 30th of the year following the reporting period. Each taxpayer must submit an individual tax return; joint returns, for example, for married couples, aren’t permitted.

One files a tax return online on the government website. The form and useful tax base information are also published there.

There is a fine for failure to file a tax return and pay the tax: it ranges between €150 and €3,000 in case there was no loss to the tax authorities. If a person underpaid the tax, the fine is 50 to 150% of the unpaid tax amount.

Corporate tax on companies’ profits

Impost de societats (IS) is the Andorran corporate tax. Both tax residents and non-resident entities pay the tax at 10%.

The 0% tax rate applies to Andorran collective investment institutions, according to Law 10/2008 dated June 12th.

Resident companies pay the tax on their global income as per their financial statements.

Non-residents are taxed on their Andorra-sourced profits only. If a non-resident entity doesn’t have a permanent establishment in Andorra, the tax is levied on a transaction-by-transaction basis.

Andorran companies can qualify for various compensations and deductions. Thus, they can reduce their corporate tax base to 0%. However, it won’t exactly be possible since January 1st, 2023: according to the new tax reform, if a company makes a profit, its minimum effective rate for the corporate tax will be 3%.

Companies must file a tax return within a month following the six-month period after the end of the accounting period. An advance payment for the current accounting period must be made on the first day of the ninth month from the start of the accounting period.

Suppose the company's accounting period starts in January and lasts 12 months. The monthly profit is €1,000,000. Thus, the annual income is €12,000,000. Let’s see when the company must pay the corporate tax and what part of the profit.

Payment schedule example for the corporate tax on €12,000,000 of the annual profit

January 1st

The beginning of the accounting period, i.e. the tax year

September 1st

The advance payment: 10% of the €8,000,000 earned from January 1st till August 31st of the same year

December 31st

The end of the accounting period, i.e. the tax year

Within the following July

Six months after the end of the tax year: 10% of the €4,000,000 earned from September 1st and December 31st of the accounting period

Required forms for financial records and tax returns are published on the government website. In addition, entities log in and file their tax returns online.

Like natural persons, legal entities bear the same penalties for tax regime violations. They pay €150 to €3,000 if they fail to file a tax return and pay taxes, but there was no loss to the tax authorities. Underpayment is charged with 50 to 150% of the unpaid liability.

Andorra has the lowest VAT in Europe

Impost general indirecte (IGI) , the Andorran value-added tax, is levied on goods, services and imports of those. However, an entrepreneur or professional isn't considered a VAT payer if the annual value of delivered goods and rendered services doesn't reach €40,000. For agricultural activities, the threshold is €150,000 per year.

The standard VAT rate is 4.5% in Andorra. It is the lowest standard rate in Europe: the second lowest is 7.7% in Switzerland.

In the EU, the standard rate cannot be below 15%. For example, Andorra's neighbours Spain and France charge 21% and 20% VAT, respectively.

Besides the standard rate, Andorra has several reduced rates, which apply to specific goods and services. An incremental rate applies to financial and banking services.

VAT rates and their application

To start paying VAT, one must register with the tax service of Andorra. Filing of tax returns is available online.

The payment schedule consists of several instalments based on a biannual, quarterly or monthly basis. The frequency of payments depends on the taxpayer’s annual turnover:

-

up to €250,000 — twice a year in January and July for the previous half a year;

-

€250,000 to 3,600,000 — four times in January, April, July, and October for the previous quarter;

-

over €3,600,000 — monthly in the prior month.

Property taxes in Andorra

Purchasing real estate implies paying a property transfer tax, Impuestos transmisiones patrimoniales (ITP). The total rate is 4% of the property value: 1.75 to 2.5% goes to Andorra’s government and about 2% more — to the municipality of the property’s location.

The buyer pays the transfer tax to a notary when concluding a purchase agreement.

Besides the transfer tax, the property buyer pays for notary services accounting for 0.5‑1% of the transaction amount. The services of a real estate agency cost about 5 to 10% of the property price.

Owning real estate implies paying an annual property tax. It is charged by local municipalities and traditionally called “Foc i lloc” — “fire and location”.

The municipality defines the rate, but it’s pretty low anyway: an owner pays €0.75 per square metre on average. Besides, only owners aged 18 to 65 must pay the tax.

Build-up real estate is taxed at €0.3 to 3 per square metre.

The municipality may also charge owners an infrastructure maintenance fee of €500 to 1,000 per year.

Leasing real estate is subject to tax, where the rate depends on the tax residency status. If Andorran tax residents gain income renting out properties, they pay the tax at 0.4 to 4%. Non-residents pay a flat 7.5% on the gross rental income.

Starting with January 1st, 2023, the tax rate on rental income will reduce by 2%. The rule will apply to the cases when the rental income doesn’t exceed €900 per person.

The tax due depends on the municipality where the rented property locates:

- Andorra la Vella — May;

- Encamp — January 1st to March 30th;

- Ordino — February 3rd to April 1st;

- La Massana — May;

- Escaldes-Engordany — May;

- Sant Julià de Lòria — November.

If a property has been unoccupied and vacant for more than two years, it is charged with a special tax, according to Law 3/2019.

The tax on empty properties is levied at €5.05 per square metre of the total usable area.

When declaring such a property, the owner must be able to confirm meeting at least one of the following conditions:

- the property is empty due to a change of address or health issues;

- the property is not the primary residence but the second or third for the owner, for example, used as a holiday home;

- the property’s address is used as a fiscal or business address for taxation;

- the property is related to some commercial activities;

- the property is set for sale through a real estate agency.

The sale of properties is subject to the capital gains tax, which the seller pays. The rate is 0—15%. We discuss the tax rates in detail in the chapter below.

There is no stamp duty neither for the seller or the buyer.

The most expensive properties are in Escaldes-Engordany: the price per square metre starts at €3,000. Thus, when purchasing a 100 m² apartment, you will pay an average of €12,000 of the transfer tax. The annual property tax will amount to about €75

Andorra’s capital gains tax for individuals and legal entities

On capital gains from securities and business shares. All capital gains not derived from the transfer of immovable property are taxed at 10%. Such gains are included in the personal income or corporate tax base.

However, if shares have been owned for more than 10 years, they are exempt from the tax. The same goes for cases when a person or a legal entity owns less than 25% of a company’s shares.

On transfer of qualifying participation. Individuals and companies don’t pay the capital gains tax in this case.

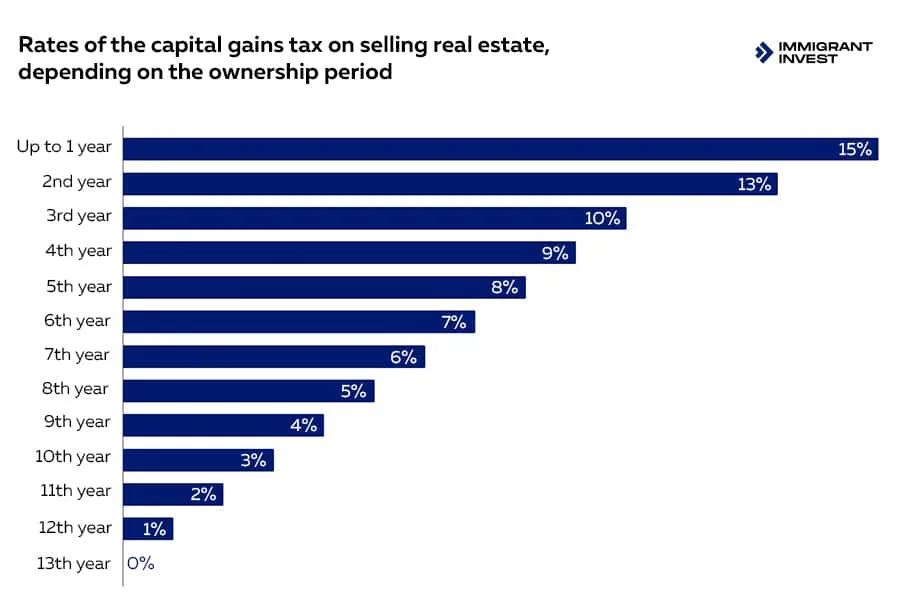

On transfer of immovable property. Natural persons and companies pay the tax both if they sell real estate.

Individuals’ capital gains from the sale of real estate may be exempt from the tax in Andorra if:

-

The property has been the primary residence, and the former owner purchased another property with the gained money within 6 months.

-

The property is located outside Andorra and has been owned for over 10 years.

When applied, the rate is progressive and depends on the ownership period: the longer you have owned the property, the lower your rate. If you’ve held the property for 13 years or longer, the tax rate is 0%.

Withholding tax on dividends, interest and royalties

The standard withholding tax rate is 10%, with an additional 1.5% on reinsurance transactions.

However, specific rules apply to income derived from dividends, interest and royalties. Besides, the withholding tax applies to fees on technical services.

Dividends are tax-free whether paid to natural persons or legal entities, tax residents or non-residents.

Interest is taxed at 10% only if paid to an individual who is an Andorran tax resident. In the case of saving account interest, the first €3,000 are exempt from the tax.

Royalties are subject to a 5% tax if paid to a non-resident individual or company. If royalties are paid to a resident individual, the tax rate is 10%. Royalties for resident companies are exempt from the tax.

Fees on technical services are taxed at 10%, except for those paid to resident companies.

Rates of the Andorran withholding tax

Other personal and business taxes in Andorra

Social contributions are paid in favour of Caixa Andorrana de la Seguretat Social, CASS. They cover medical services and pensions.

If a person gets a salary from an Andorran company, social contributions amount to 22% of the gross wage. Of these, the employee’s part is 6.5%, and the employer pays the rest, 15.5%.

Self-employed persons pay social contributions, too. However, they are subject to a fixed payment: in 2021, it was €457.88 per month. Besides, one can get a 50% concession and decrease social contributions to €228.94 per month:

-

within the first 12 months of the tax liability;

-

if the results of the previous fiscal year showed less than €12,000 of profit and €150,000 in turnover.

The vehicle ownership tax. If you import a car from any EU country, you pay a VAT of 4.5%. A car is manufactured outside the EU and is subject to a 10% tax.

Besides, a vehicle owner pays a €200 fee for a car’s registration. A licence plate costs an additional €60.

Only residence permit holders who can prove an address in Andorra can register a vehicle in the country.

Gambling is taxed at 3 to 25%, depending on the type of activity and the amount of the prize won. For example, if you win in online poker, the prize will be subject to a capital gain of savings: the first €3,000 will be exempt, and the rest will be taxed at 10%.

The exit tax is charged when a person or a company changes their tax residency from Andorran to any other. Unrealised capital gains are subject to tax. The tax amount for companies also considers their assets’ fair market and tax values.

More tax benefits and exemptions

Andorra has no taxes on wealth and inheritance. There is no capital or stamp duty.

Tax deductions are available to legal entities and individuals. Companies can reduce corporate tax amounts when they hire new employees or make new investments. Individuals may qualify for deductions if they have dependents or mortgages.

Special tax regime for holdings. If an Andorran holding company only manages and participates in non-resident companies outside the country, such a holding is exempt from taxes on:

-

dividends received from foreign subsidiaries or companies;

-

dividends paid to the holding’s shareholders, whether they are in Andorra or abroad;

-

capital gains earned by transferring shares.

A shareholder, a person or a company, doesn’t pay an income or corporate tax on the dividends received from a holding.

To become subject to this special tax regime, a holding company must apply and get an authorisation from the Andorran tax service.

Operational losses. A company can carry them forward for up to 10 years without the carryback.

Ways to start paying taxes in Andorra

Relocation to Andorra is the way to become a tax resident: one must spend more than 183 days a year in the country to register as a taxpayer.

Living in Andorra for more than half a year is only possible with the country’s residence permit or passport. A foreigner must obtain active or passive residency status to relocate to Andorra.

Active residency implies that the holder will live and work in the country. It is granted to:

-

Self-employed applicants must own at least 11% of a company registered in Andorra and act as managing directors. There is a quota of 900 residence permits per year for self-employed. Besides, their family members can get residence permits only 12 months after the main applicant.

-

Specialists who get hired by a local company.

The first active residence permit is valid for a year, with the right to extend it. After 20 years of living in Andorra, a resident can apply for citizenship.

Passive residency is designed for those who want to live in the country, but the centre of their economic activity will remain abroad. This path might suit international businessmen, athletes, artists, scientists, and other professionals.

Investors are offered a unique path to residency in Andorra. Investments of at least €400,000 must be made in the country's economy:

-

€350,000+ — Investments in property, securities, investment funds, businesses, or interest-free deposits;

-

€50,000+ — Deposit with Autoritat Financera Andorrana, AFA.

However, the investment amount might increase in the future if the Government of Andorra accepts proposed changes to the rules of issuing residence permits to real estate investors. Under new terms, a minimum investment of €400,000 will be required when purchasing public housing. In other cases, the investment amount will be €600,000.

Spouses and children under 25 can get residence permits simultaneously as an investor.

The first passive residence permit is granted for two years with the right to extend it. Investors must spend at least 90 days a year in Andorra to maintain residency. However, citizenship application becomes available only after 20 years of permanent living in the country.

Registration of a company in Andorra takes about two months. After that, the company becomes an Andorran tax resident.

There are two types of companies one can register:

-

Public Limited Company — Societata anònima, SA. The minimum nominal capital is €60,000. The capital can be distributed among shareholders or held by one person. In the latter case, the company type is a Sole-Shareholder Public Limited Company — Sociedad anónima unipersonal, SAU.

-

Private Limited Company — Societat limitada, SL. The minimum nominal capital is €3,000. It also can be a Sole-Shareholder Private Limited Company — Societat limitada unipersonal, SLU.

First, you send a request to the government to reserve a corporate name: the reservation certificate is valid for six months. During this time, you get an authorisation for the transfer of foreign investments to Andorra, open a local bank account, and prepare and notarise a deed of the company’s incorporation.

When all requirements are met and documents prepared, you register the business with the Andorran Company Registry and the Registry of Trade and Industry.

If you want to establish an office in Andorra, an electrical inspection certificate and a valid contract for fire extinguishers are required.

Is it possible not to pay taxes twice after becoming a tax resident of Andorra?

Andorra has double taxation treaties (DTTs) with 10 countries:

-

France.

-

Spain.

-

Portugal.

-

Luxembourg.

-

Liechtenstein

-

The United Arab Emirates.

-

Malta.

-

Cyprus.

-

San Marino.

-

Hungary.

The DTTs set foreign tax credit rules in case of income, corporate, capital gains, and withholding taxes.

Thus, suppose a person is an Andorran tax resident but receives income from one of the listed countries, for example, France. They pay the personal income tax in the source country, i.e. in France, and provide the Andorran tax service with documental proof of the paid taxes. Andorra will count the tax as already paid, and no double taxation will arise.

If the source country doesn’t have a DTT with Andorra, an individual or a company has to pay taxes twice, both in the source country and Andorra.

Immigrant Invest is a licensed agent for citizenship and residence by investment programs in the EU, the Caribbean, Asia, and the Middle East. Take advantage of our global 15-year expertise — schedule a meeting with our investment programs experts.